Do we see a tipping point?

A bit of a spoiler to start with: For the first time since the cost-of-living-crisis started, shoppers seem to see a silver lining. Looking at the latest survey and report, we analyzed five aspects to substantiate the initial signs for a tipping point, exploring

1how the permacrisis is affecting the shoppers’ state of mind as well as their mindset,

2 to what extent this is translating into shifts in grocery shopping strategies,

3 how buying preferences are evolving, especially with regards to brands and private labels,

4 whether this tipping point also affects retailer choice and strategy, and finally,

5 whether we can expect shifts in greater lifestyle needs and respective changes that shoppers seek.

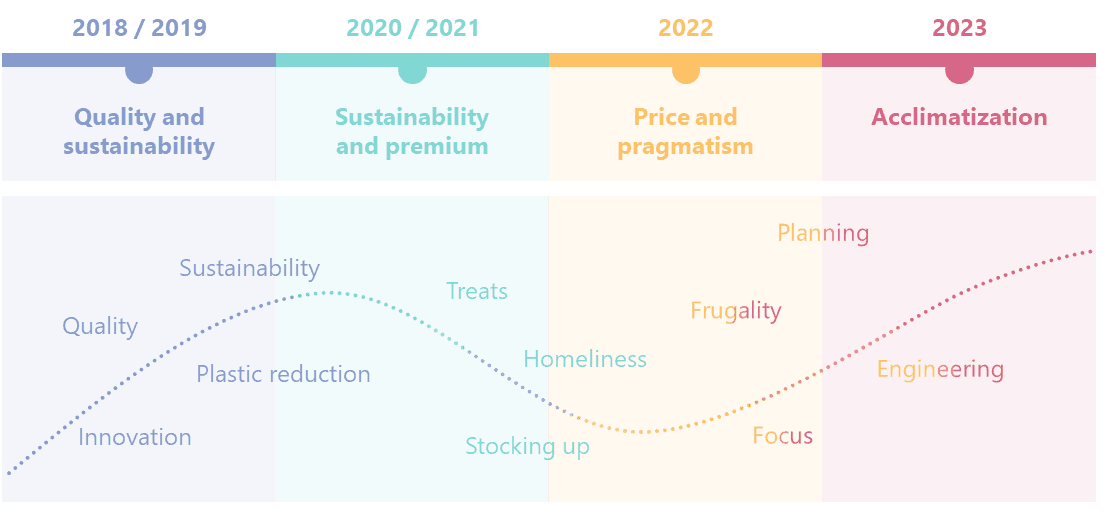

Shoppers take and learn something from every crisis. Looking at last year, we observe acclimatization and engineering: Shoppers implemented new habits to handle their basics. They have overcome the panic phase of inflation and are managing their budgets to make sure they can really buy what they cannot do without. Besides the basics, this also includes key lifestyle products, whereas nice-to-haves have been reduced.

2023 saw nearly 900 million additional shopping trips across Europe (+3%) as shoppers were forced to shop around for the best bargains. Half of all categories have lost volume compared to pre-COVID, and three quarters have lost volume compared to last year.

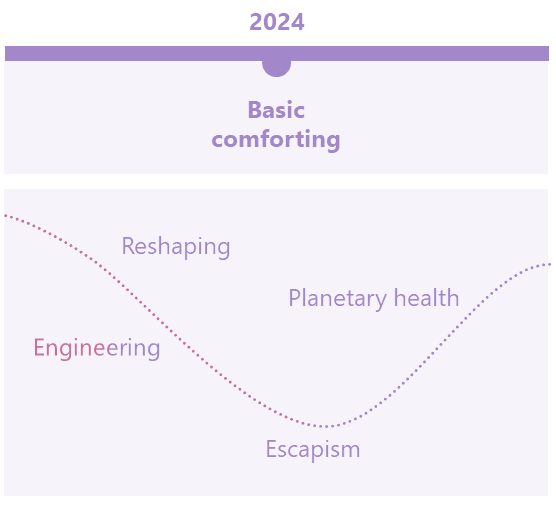

The past years have seen a lot of shuffles in behavior, which will settle a bit into a new mode, and shoppers will again reshape their behaviors. With the peak of shopping around and rationalizing behaviors behind us, this reshaping will translate into budget engineering to make room for small treats or little extras, albeit in a very budget-sensitive way. In a still very complex and unsecured social context, “escapism” promises to provide some comfort and good feeling.

Unless there is a major systemic shock, we believe that the near future will be marked by “basic comforting”.

External factors have become more complex over the past years, creating a lot of insecurity and an increasing number of concerns competing for attention.

So, what keeps shoppers awake at night and what do they expect for the months ahead?

Not surprisingly, economic concerns continue to be top of mind, but have decreased since spring 2023. With the panic phase behind us, other concerns have “re-emerged”, including worries about the environment, personal physical and mental health, and social inequality. As a result, sustainability is back on the agenda – after a small glitch in the panic phase –, but will take a new direction: Planetary health is becoming an aspiration and we will explore this topic further in the context of lifestyle changes.

A shortage of energy supplies is more or less the only worry that has been declining noticeably, which confirms the increase in complexity of concerns.

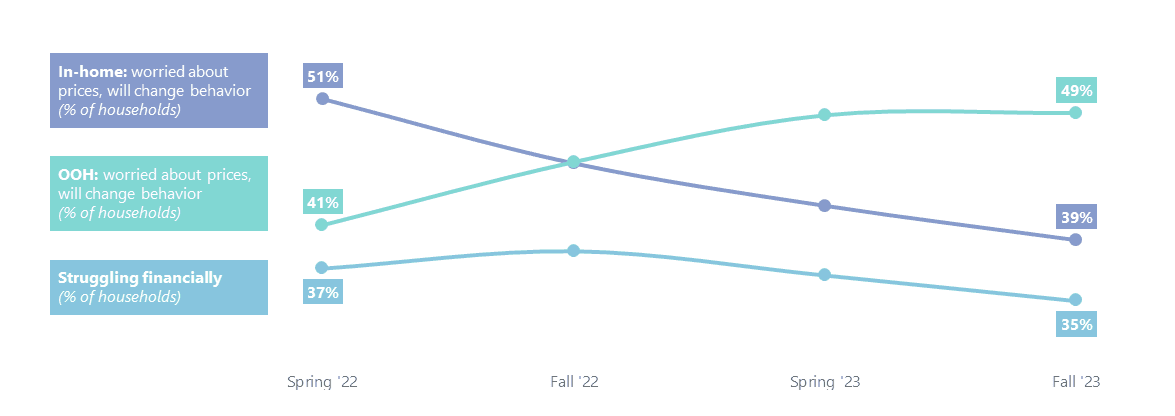

A bit of good news: Overall, less households across Europe are struggling financially. Especially in The Netherlands, Denmark and Germany, four out of ten households have comfortable budgets. At the same time, in certain countries more than 50% of households continue to be in a financially difficult situation, foremost in Spain, Hungary and Serbia. However, all in all, only four countries are doing less well than half a year ago, when it comes to budget wiggle room, including the UK and Italy, so the direction of change for most countries is positive.

As shoppers’ financial worries are decreasing, we observe a turn in adaptive behaviors. Concerns about “in-home” prices including groceries have dropped considerably, but shoppers still worry about the “extras”, especially their out-of-home (OOH)-expenditures. Further intended behavior change when shopping for daily necessities – as a result from high inflation – is the lowest in Denmark (33%) and the highest in Hungary (48%).

Sources1 - CPS GfK Consumer Panel data EU-16 ; MAT Q2 2023 vs MAT Q2 20222 - Europanel FMCG barometer, Q1 2023 vs 2022/2019; 1065 categories in DE, ES, FR, IT, NL, UK

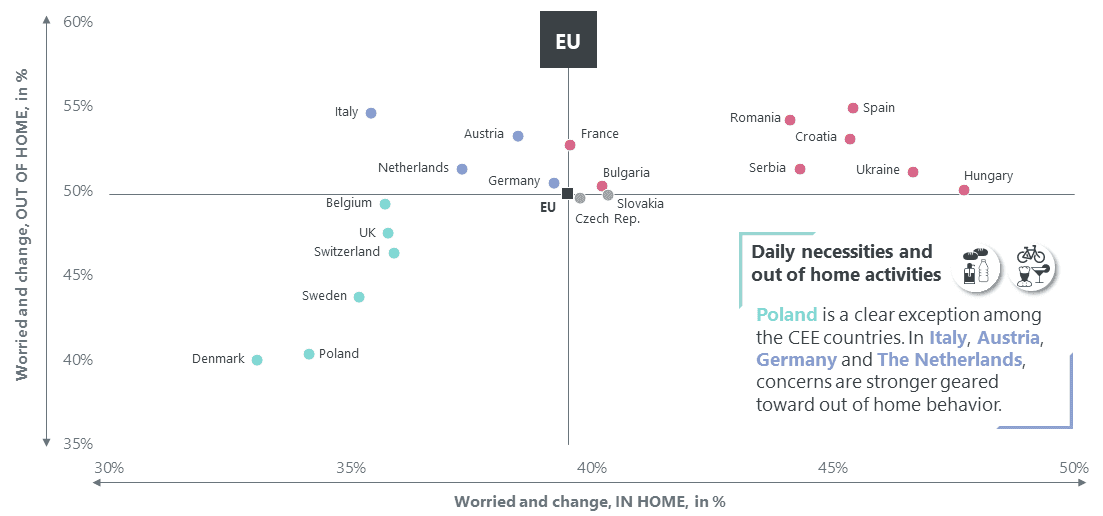

In general, there is a fairly distinct split between the countries of Central and Eastern Europe (CEE) and those in Western Europe (WSE): With the exception of Poland, shoppers in Eastern European countries worry much more about the prices of daily necessities, expecting to change their behavior for both in-home and OOH. In Western Europe, worries concerning in-home purchases are fading, but shoppers in Italy, Austria, the Netherlands, and to a lesser extent, Germany, still fear for the need to adapt their OOH expenditures.

Generally speaking, the outlook of shoppers in 2024 can be described as cautiously optimistic.