Brands have the opportunity to regain trust

The cost-of-living crisis has played very much in favor of private labels (PL), with shares now at record levels: In Western Europe, PL reached a high of 41% in late 2023 (*). But if we were on a level playing field and the price was the same, more than half of the shoppers (54%) would opt for brands: 51% state that buying private labels is a pure budget decision. And make no mistake, it is a deliberate decision, as 52% consciously buy PL or a brand, and for just 18% it does not seem to make any difference.

The vast majority also plans to stick to their new learned habits (61%) in 2024: 32% intend to buy even more PL, and only eight percent plan to buy more brands. Brands still need to work extremely hard to re-gain shoppers, but currently have a window of opportunity to do so, not only because of the relaxation described above: Shoppers still feel that brands provide better quality and innovation. Private labels will have to raise the bar, especially when it comes to product standards and eco-claims.

More than every second launch comes from a brand, so their reputation of being the better innovators is not unfounded. But after years of slowed activity during the permacrisis, pressure is on to once again raise the level of innovation. Shoppers have grown skeptical towards brands; trust and credibility need to be rebuilt.

In times of price focus and “promo-hopping”, launches are extremely important to break the downward pricing spiral and create new benefits that justify higher prices: Six in ten launches sell at a price above the parent brand, ranging from eight percent price premium in food to as much as a plus of 43% in home care.

(*) Source: Europanel Barometer

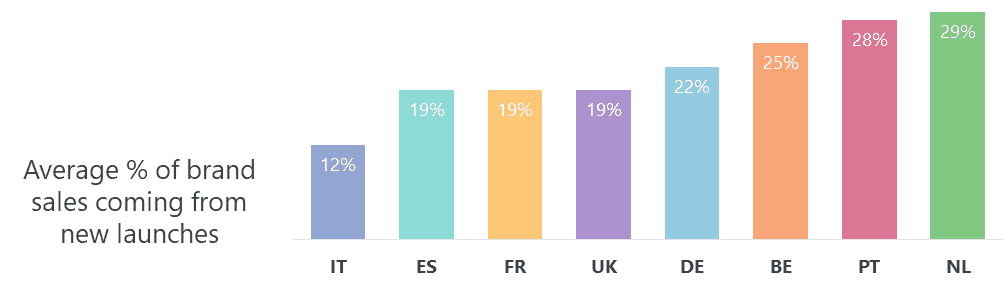

Looking at country specifics, Dutch shoppers seem to be especially receptive to launches, as 29% of brand sales derives from innovation.

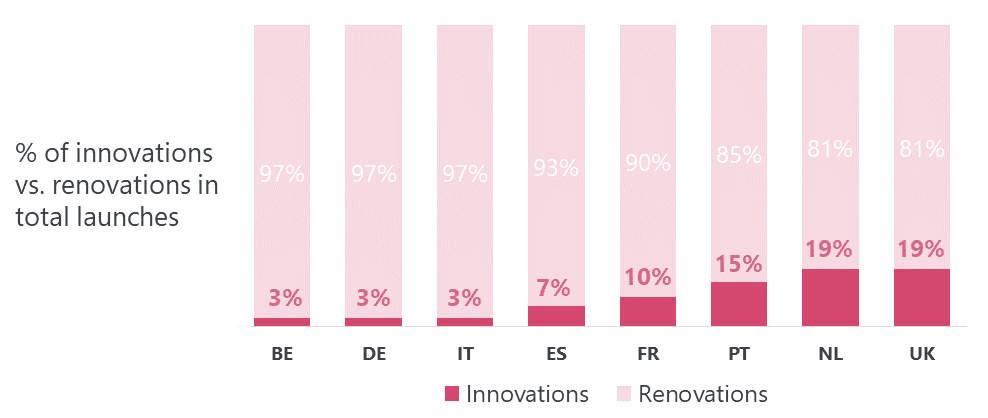

A matter of necessity or quality? With the Netherlands having an especially high PL share, brands are forced to differentiate. About 19% of launches in The Netherlands are viewed as true innovations, compared to a mere three percent in Belgium and Germany. Private labels not necessarily impede brands to grow, but launches make an important difference.

With an average number of 121 launches per year, the frequency of launches is higher in categories with a high penetration (above 65%), but the success is lower – with an average reach indexed at 0.7 one quarter after a launch. Especially in times of budget squeezes, shoppers question the justification of a higher price, just for a new flavor or a little less sugar. On the other hand, less “launch noise” in less frequency categories (38 vs. 133 in high frequency categories) still gets more attention, leading to higher success rates in terms of launch reach (index: 1.3). However, launches in categories with a low penetration have to provide real value-add: As shoppers will not buy the new product on a high frequency, they cannot afford to make a mistake.

With more shelf competition from private labels, launches also have to be incremental to the respective category to mitigate sometimes conflicting retailer interests. A good example of adding value and growing a category is cereals: Quite basic products, such as traditional oatmeal, have evolved over the years into different added-value offerings, including muesli, porridge, and overnight oats, resulting in significant category growth in volume and value.

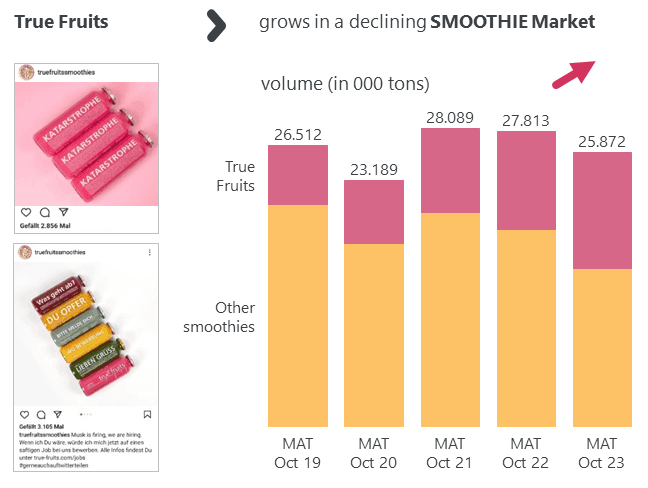

Even (or a fortiori) if a brand is part of a small, less frequent category, it pays off to constantly invest in innovation and creative communication, also to mitigate negative category developments. A very good example is True Fruits, a high-priced product nonetheless showing high brand loyalty, and still growing in the declining category of smoothies.

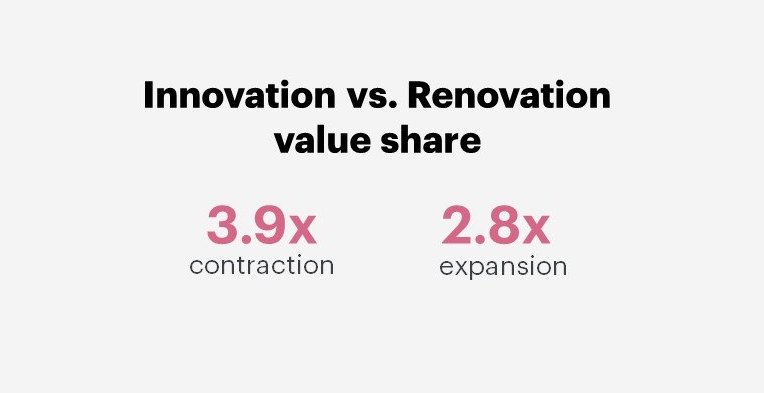

The notion of countercyclical investment is not new. Research shows that it is essential to invest in tough times to ensure long-term survival. Brands which increased research and development (R&D) at the expense of advertising in times of economic contraction, were able to increase their market share by 38% and their profits by 70%. True innovations pay off much more than renovations, especially in times of contraction, when shoppers are willing to spend their “last euro” only on something worthwhile.

Constant innovation is just as essential in trending categories such as vegan and vegetarian food. Of course, categories like dairy, meat, and cheese alternatives are still growing, but private labels have caught up, and more often first-mover brands are now suffering. By contrast, in a newer category such as vegan sweets, first-mover brands can still generate considerable growth rates.

The need for frequent innovation applies to many different categories, as we now observe the “return” of some key product trends such as convenience, health, sustainability, and lifestyle / premium. Interestingly enough, these trends are nowadays primarily driven by private labels.

Brands need to credibly unite function, hedonism, and sustainability to make a real difference – serving just one trend does not cut it.

This is clearly the time for transformation. Renovations are not good enough, innovation counts – innovation, incremental to the needs of shoppers and therefore to the category.